Emergency Fund Strategy: How Much You Actually Need

An emergency fund is a cash reserve set aside to cover unexpected expenses or income disruptions — job loss, medical bills, car repairs, or home emergencies. It is not an investment. Its purpose is liquidity and protection, ensuring you don't need to sell investments at a loss or take on high-interest debt during a financial disruption. According to the Consumer Financial Protection Bureau, most financial professionals recommend holding 3–6 months of essential expenses in a high-yield savings account.

TL;DR

Keep 3–6 months of essential expenses in a high-yield savings account (HYSA) earning 4–5% APY. If your monthly essentials are $3,500, your target is $10,500 to $21,000. Build it in stages — start with $1,000, then one month of expenses, then three, then six. Use a separate HYSA at a bank like Marcus, Ally, or Wealthfront so the money isn't mixed with everyday spending. Automate a recurring transfer each payday. Build your emergency fund before investing aggressively — it's the foundation that protects everything else.

The Framework

Calculate your baseline monthly expenses. Add up non-negotiable costs: rent/mortgage, utilities, groceries, insurance premiums (compare car insurance | compare homeowners insurance | compare life insurance), minimum debt payments, transportation. Exclude discretionary spending. This is the number you'd need to survive if income stopped.

Set your target: 3 months (minimum) or 6 months (recommended). 3 months is appropriate for dual-income households with stable employment. 6 months is more suitable for single-income households, self-employed individuals, commission-based earners, or anyone in an industry with higher layoff frequency.

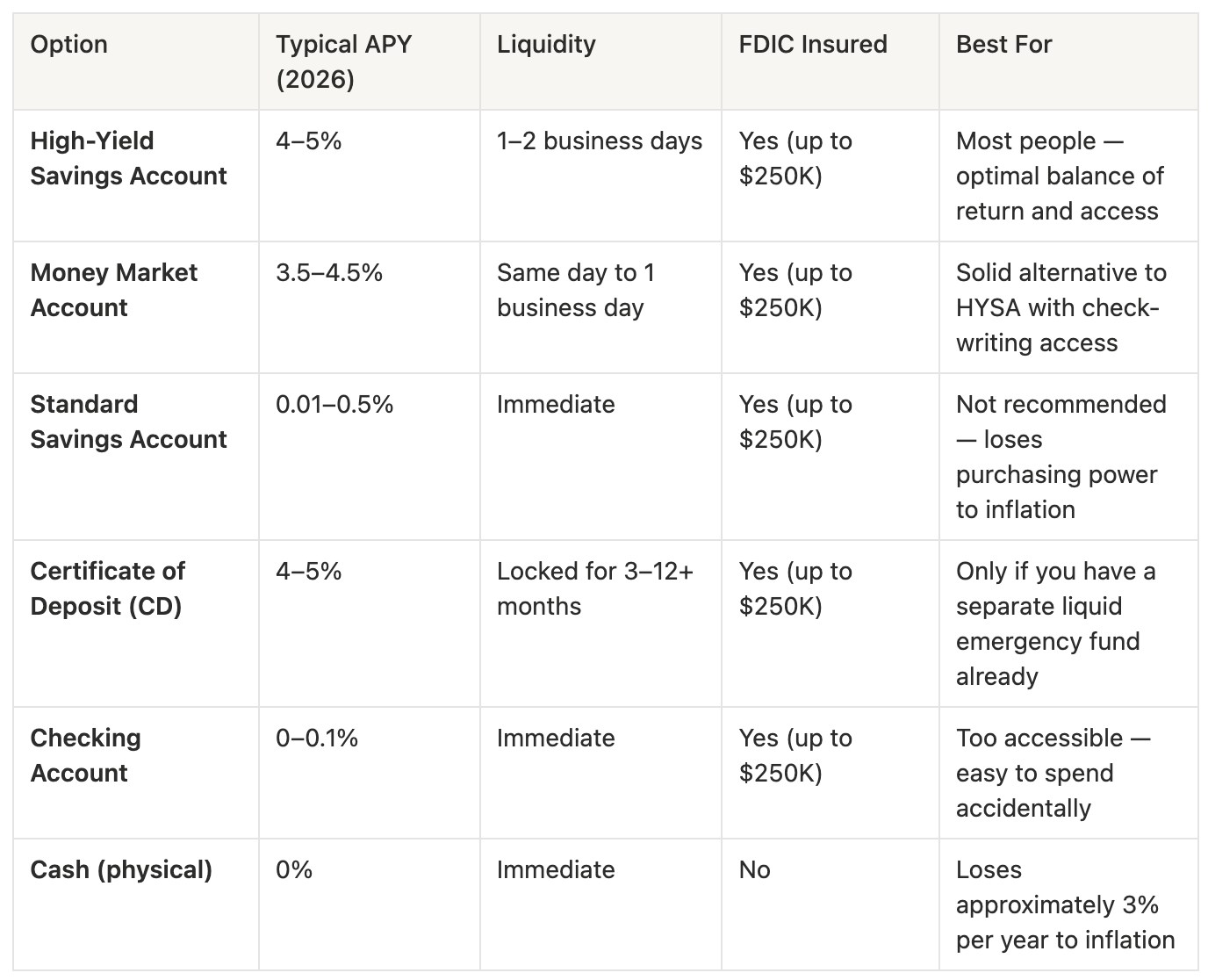

Use a high-yield savings account. According to FDIC data, as of 2026, competitive HYSAs offer 4–5% APY. On a $15,000 emergency fund, that produces $600–$750/year in interest. A standard savings account at a major bank typically earns 0.01–0.5% — a significant difference over time. (Compare high-yield savings accounts) (FDIC: National Rates and Rate Caps)

Build in stages. Start with a $1,000 starter fund. Then build to one full month of expenses. Then three months. Then six. Attempting to save $15,000–$20,000 immediately is unrealistic for most households and leads to abandoning the goal.

Automate and separate. Set up a recurring transfer from your checking account to your HYSA on each payday. Even $50–$100 per paycheck adds $1,300–$2,600/year. Keep the emergency fund in a separate bank from your daily spending accounts to reduce the temptation to dip into it for non-emergencies.

Comparison Table: Where to Keep Your Emergency Fund

Who is this for?

Anyone who does not yet have 3–6 months of expenses saved in a liquid, accessible account

People who have experienced financial emergencies that forced them into debt

Households with variable or commission-based income

Single-income families or sole providers

Individuals who want to begin investing but need a financial safety net first

FAQ

Should I invest my emergency fund in the stock market?

In most cases, no. The purpose of an emergency fund is immediate, reliable access without market risk. The stock market can decline 20–30% during the same period you experience a job loss or emergency. Keeping the fund in a HYSA preserves the capital while still earning interest.

Is 3 months enough or do I need 6?

3 months is a reasonable starting target for dual-income, stable-employment households. 6 months is more appropriate if you're self-employed, a single earner, in an industry with frequent layoffs, or have dependents. When uncertain, targeting 6 months provides a wider safety margin.

Should I build my emergency fund before paying off debt?

Start with a $1,000 minimum emergency fund, then focus on high-interest debt (credit cards, payday loans). Once high-interest debt is eliminated, build the full 3–6 month fund before shifting to aggressive investing. Without an initial buffer, one unexpected expense can restart the debt cycle.

Where should I open a high-yield savings account?

Marcus by Goldman Sachs, Ally Bank, Wealthfront, Capital One 360, and SoFi are commonly cited options with competitive APYs, no monthly fees, and no minimum balance requirements. Compare current rates, as they fluctuate with the federal funds rate. Opening an account online typically takes 5–10 minutes. (Compare high-yield savings accounts)

What qualifies as a real emergency?

Job loss, unexpected medical expenses, essential car or home repairs, and urgent family situations. Planned expenses (holidays, vacations, annual subscriptions) are not emergencies — those should be handled through a separate sinking fund. A sale or limited-time deal is not an emergency.

What if I need to use my emergency fund before it's fully built?

Use it. That's what it's for. Then make rebuilding it your top financial priority before resuming aggressive investing or discretionary spending. A partially funded emergency fund is substantially better than none.

Related Guides

The Order of Investing: Where to Put Your Money First — Once your emergency fund is built, here's where to invest next

The Paycheck Split System — Automate emergency fund contributions using the 50/30/20 framework

Debt Payoff Strategy — How to balance debt payoff and emergency fund building

Sources

Federal Reserve: Survey of Household Economics and Decisionmaking (SHED)

Consumer Financial Protection Bureau: Building an Emergency Fund

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation. Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you if you click through and take action. We only recommend products and services we believe are genuinely useful.