The Paycheck Split System: How to Budget Without a Spreadsheet

The paycheck split system is an automated budgeting method that divides each paycheck into three categories, needs, wants, and savings/investing, using separate bank accounts and automatic transfers. According to the Consumer Financial Protection Bureau, it is based on the 50/30/20 framework and designed for people who want structure without daily expense tracking. The system runs on automation, which means it requires initial setup but minimal ongoing effort.

TL;DR

Split every paycheck into three buckets the day it hits your account: approximately 50% to needs (rent, bills, groceries), 30% to wants (dining, entertainment, personal spending), and 20% to savings and investing (emergency fund, 401(k), Roth IRA). Set up automatic transfers and auto-pay for recurring bills. Use separate bank accounts for each category. When the spending account is empty, discretionary spending stops until the next paycheck. No tracking individual purchases. No spreadsheets. The system works because it removes daily decision-making from the equation.

The Framework

Set up automatic transfers on payday. The moment your paycheck deposits, automatic transfers should move money to your bills account, savings account, and investment accounts. What remains in your checking account is your discretionary spending for the period.

50% to needs. Rent/mortgage, utilities, insurance premiums (compare car insurance | compare homeowners insurance | compare life insurance), groceries, minimum debt payments, transportation. If your needs consume more than 50%, that's a signal to examine your largest fixed costs — typically housing — or to focus on increasing income.

30% to wants. Dining out, entertainment, clothing, subscriptions, hobbies. This is guilt-free spending because the essential categories are already funded. Spending within this bucket doesn't require justification.

20% to future wealth. 401(k) contributions, Roth IRA, emergency fund, additional debt payments beyond minimums. This is the wealth-building allocation. For context, 20% of a $60,000 gross salary is $12,000/year or $1,000/month across all savings and investment accounts.

Use separate bank accounts. One checking account for fixed bills (auto-pay everything from here). One checking account or debit card for discretionary spending. One high-yield savings account for emergency fund and short-term goals. (Compare high-yield savings accounts) Physical separation between accounts makes overspending structurally difficult.

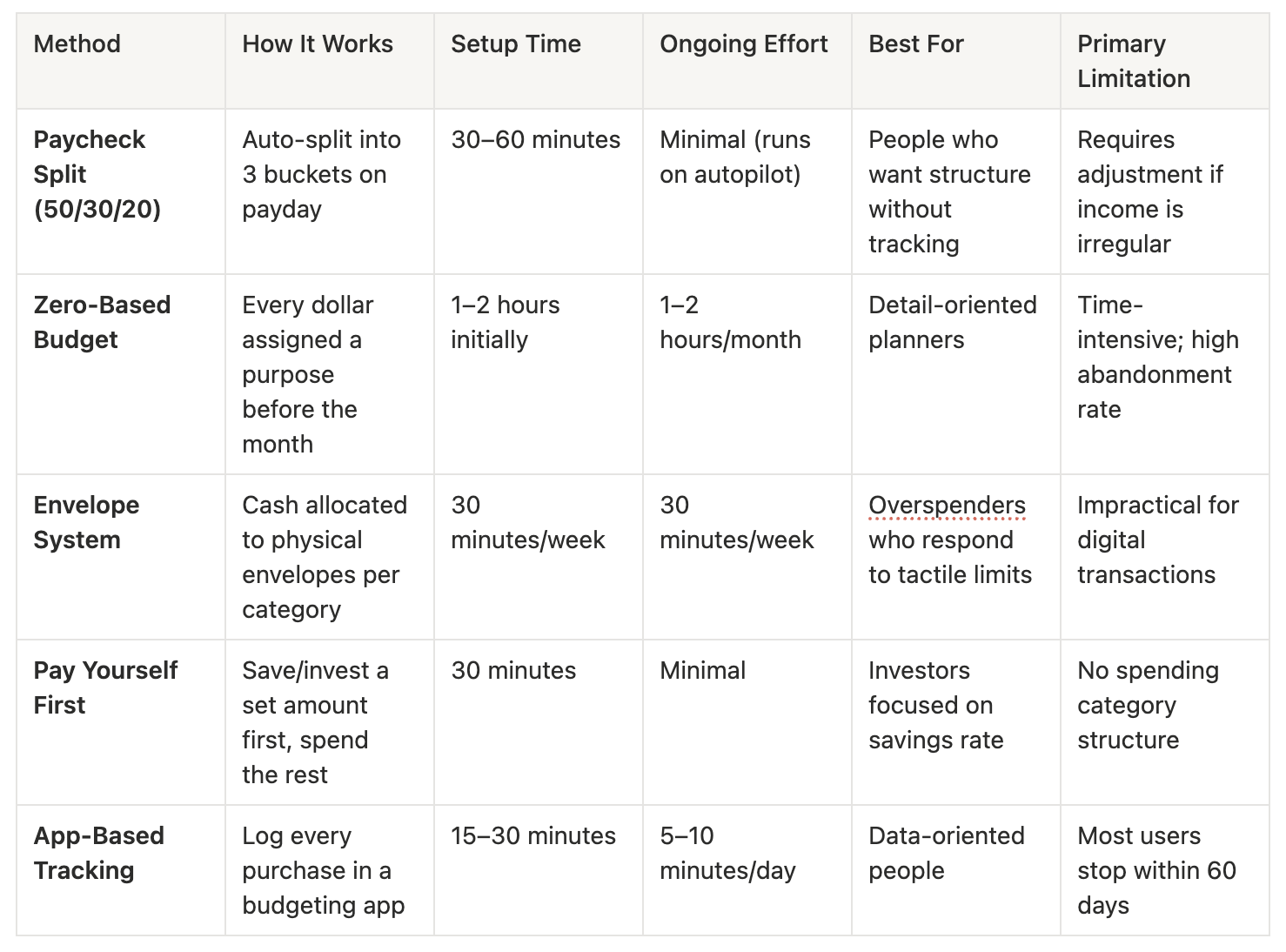

Comparison Table: Budgeting Methods

Who is this for?

People who have tried and abandoned detailed budgets or expense-tracking apps

Anyone who wants a functional system that requires minimal ongoing maintenance

Households with consistent, predictable income (salaried employees, steady hourly workers)

People who tend to overspend when money sits in a single checking account

Anyone looking for a starting framework they can adjust as their income or expenses change

FAQ

What if my needs are more than 50% of my paycheck?

Adjust the ratios to fit your current reality. 60/20/20 or even 70/15/15 may be necessary depending on housing costs and debt obligations. The goal is to have a system, not a perfect ratio. As income increases or fixed costs decrease, move closer to 50/30/20.

Which bank accounts should I set up?

At minimum: one checking account for bills (all fixed expenses auto-pay from here), one checking account or debit card for everyday discretionary spending, and one high-yield savings account for your emergency fund. Some people add a separate savings account for short-term goals (vacation, car repair fund).

How do I handle irregular expenses like car maintenance or holidays?

Create a sinking fund within your savings. Set aside $100–$200/month for predictable but non-monthly expenses — car maintenance, holiday gifts, annual insurance premiums, back-to-school costs. These are not emergencies; they are foreseeable expenses that should be planned for.

Does the 20% savings include my 401(k) contribution?

Yes. The 20% includes all savings and investing: 401(k) contributions, employer match, Roth IRA contributions, emergency fund deposits, and any additional investment account contributions. If your 401(k) already takes 10% of your gross pay, the remaining 10% goes to your Roth IRA and savings.

What if my income is variable or commission-based?

Use your lowest reliable monthly income as the baseline for your 50/30/20 split. In higher-income months, direct the excess to savings, investing, or debt payoff. This prevents overspending during good months and ensures essentials are covered during lean months.

I've tried budgeting before and stopped. Why would this work?

The system removes the most common failure points: daily tracking, categorizing individual purchases, and willpower-based spending decisions. Once set up, it runs automatically. The only rule is that when the discretionary spending account is empty, spending stops until the next paycheck. That constraint is structural, not motivational.

Related Guides

Emergency Fund Strategy: How Much You Actually Need — How much to put in that savings bucket and where to keep it

The Order of Investing: Where to Put Your Money First — What to do with the 20% that goes to future wealth

How Much Should I Invest Per Month? — Turn your savings percentage into a specific monthly dollar target

Sources

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation. Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you if you click through and take action. We only recommend products and services we believe are genuinely useful.