The $3 Million Retirement Math (Broken Down)

The $3 million retirement number is a specific savings target based on the 4% withdrawal rule — the idea that withdrawing 4% of your portfolio annually has historically sustained a 30-year retirement in most market conditions. $3 million at 4% produces $120,000/year ($10,000/month) in retirement income. This guide breaks down exactly how much you need to invest each month to reach that target, depending on when you start and what returns you can reasonably expect.

TL;DR

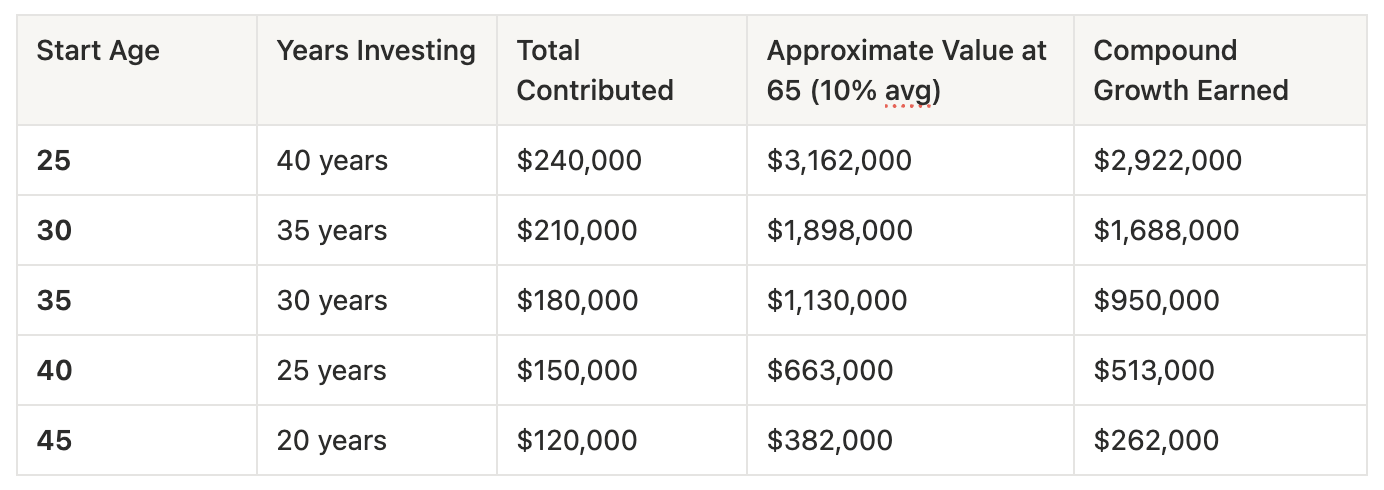

Retiring with $3 million requires consistent investing over time, not a high salary. At a 10% average annual return (the historical average of the S&P 500), investing $500/month starting at age 25 grows to approximately $3.16 million by age 65. Start at 30 and the same $500/month reaches roughly $1.9 million. Start at 35, approximately $1.13 million. The earlier you start, the less of your own money you need to contribute — compound interest does most of the work. The 4% rule applied to $3 million produces $120,000/year in retirement income.

The Framework

Understand the math. $500/month invested at 10% average annual return for 40 years grows to approximately $3.16 million. Of that, only $240,000 is your own contributions. The remaining $2.92 million comes from compound growth. Time is the primary variable, not income level.

Time matters more than amount. $500/month starting at 25 produces more than $1,000/month starting at 35 — even though the later investor contributes more total dollars. A 10-year head start with lower contributions outperforms a later start with higher contributions in most scenarios.

Use tax-advantaged accounts first. Maximize your 401(k) match, then your Roth IRA ($7,500 in 2026), then increase 401(k) contributions ($24,500 limit in 2026). Tax-advantaged growth means more of your returns stay invested rather than going to taxes each year. (Compare online brokerages) (IRS: 2026 contribution limits)

Use the 4% rule to find your number. Multiply your target annual retirement spending by 25. $80,000/year = $2 million needed. $120,000/year = $3 million. $50,000/year = $1.25 million. The 4% rule is based on the Trinity Study, which tested historical withdrawal rates across multiple market conditions. (Trinity Study — AAII)

Automate and stay consistent. Set up automatic monthly investments. Historically, investors who maintained consistent contributions through market downturns have outperformed those who tried to time their entry points. The strategy is consistency, not prediction.

Comparison Table: What $500/Month Becomes

Figures assume 10% average annual return compounded monthly. Actual returns will vary. These are estimates for illustrative purposes.

Who is this for?

Anyone who wants a specific, math-based retirement savings target

Investors in their 20s or 30s who want to understand how much monthly investing can produce over time

People who feel overwhelmed by retirement planning and want a clear number to work toward

Households that want to understand how starting age impacts their final portfolio value

Anyone wondering whether $3 million is realistic on a middle-class income

FAQ

Is a 10% average return realistic?

According to historical data compiled by Macrotrends, the S&P 500 has returned an average of approximately 10% per year over the last 50+ years, including multiple recessions and market crashes. However, this is a long-term average — individual years vary significantly (some up 25%+, some down 30%+). For planning purposes, many financial professionals use 7–10% for long-term projections. Using 7% (inflation-adjusted) is more conservative.

What if I can't invest $500/month right now?

Start with what you can. $100/month from 25 to 65 at 10% average return grows to approximately $632,000. $200/month reaches roughly $1.26 million. The specific amount matters less than the consistency. Increase contributions as income grows — particularly when you receive raises or pay off debts.

Do I actually need $3 million to retire?

It depends on your expected annual spending. The Rule of 25 (annual expenses x 25) provides a baseline: $60K/year needs = $1.5 million. $80K/year = $2 million. $120K/year = $3 million. $40K/year = $1 million. Calculate based on your actual anticipated expenses, not a generic target.

What about inflation?

Inflation has averaged approximately 3% per year in the U.S. over the last century. A 10% nominal return minus 3% inflation equals roughly 7% real return. At 7%, $500/month for 40 years grows to approximately $1.31 million in today's purchasing power. Still significant, and the 4% rule's original research accounted for inflation adjustments in its withdrawal methodology.

What if the market crashes right before retirement?

This is known as sequence-of-returns risk. The standard mitigation is to shift your asset allocation toward more conservative holdings (bonds, cash equivalents) as you approach retirement. At age 25, a portfolio heavily weighted in equities is appropriate given the long time horizon. By ages 55–60, incorporating bonds and stable-value funds helps protect accumulated gains. Target-date funds automate this transition.

Does the 4% rule still work?

The original Trinity Study found that a 4% initial withdrawal rate, adjusted annually for inflation, survived 95% of historical 30-year periods. Some current financial planners recommend 3.5% for additional safety margin, especially for retirements expected to last longer than 30 years. This would mean multiplying annual expenses by approximately 28.5 instead of 25.

Related Guides

The Rule of 25: How to Know Your Retirement Number — Calculate your exact retirement target using the 4% withdrawal rule

How Much Should I Invest Per Month? — Work backwards from your $3M target to a monthly contribution amount

Index Fund Investing 101 — The investment vehicle that makes the $3M math work

Sources

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation. Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you if you click through and take action. We only recommend products and services we believe are genuinely useful.