Debt Payoff Strategy: How I Paid Off $230K

A debt payoff strategy is a structured plan for eliminating debt by prioritizing which debts to pay first, finding additional money to accelerate payments, and maintaining a system until all balances reach zero. The two most common approaches are the avalanche method (highest interest rate first) and the snowball method (smallest balance first). Both work — the difference is whether you optimize for total interest saved or for psychological momentum. The right method is the one you can sustain.

TL;DR

List every debt with its balance, interest rate, and minimum payment. Choose either the avalanche method (pay the highest interest rate first to save the most money) or the snowball method (pay the smallest balance first for quicker wins). Make minimum payments on everything, then direct all extra cash toward your target debt. Keep a $1,000 emergency buffer while paying off debt to avoid re-entering the debt cycle. Find extra money through subscription audits, selling unused items, and directing bonuses or tax refunds to debt. Track progress visually. Consistency matters more than speed.

The Framework

List every debt. Name, balance, interest rate, and minimum monthly payment for each. Include credit cards, student loans, car loans, personal loans, and medical bills. Seeing the full picture — even if it's uncomfortable — is the starting point for a workable plan.

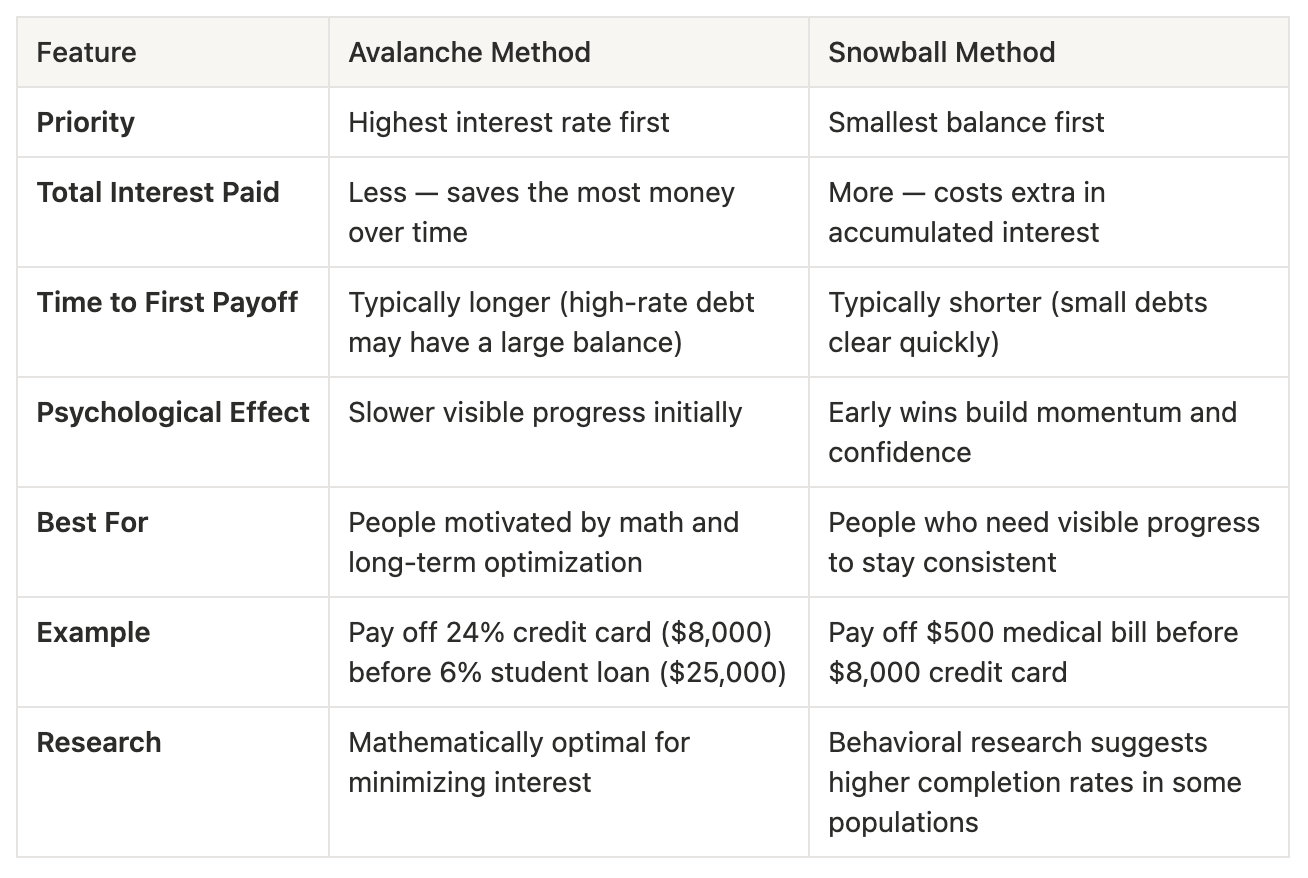

Choose your payoff method. According to research published in Harvard Business Review, the avalanche method (highest interest rate first) minimizes total interest paid over time, while the snowball method (smallest balance first) provides faster initial wins that can help sustain motivation. Both approaches are mathematically superior to making only minimum payments. (Harvard Business Review: Research on Debt Repayment)

Redirect all available extra cash to the target debt. Audit subscriptions, reduce discretionary spending, sell unused items, and direct windfalls (tax refunds, bonuses, side income) to debt. If you owe back taxes, addressing that can also free up monthly cash flow. (Explore tax relief options) An extra $200–$400/month can reduce a payoff timeline by years and save thousands in interest.

Maintain a $1,000 emergency buffer. Not a full 3–6 month fund — just $1,000. This prevents a single unexpected expense from forcing you back into debt while you're paying it down. Build the full emergency fund after high-interest debt is eliminated.

Track your progress. Use a debt tracker spreadsheet, app, or visual chart. Seeing balances decrease over time provides measurable evidence that the strategy is working. This is particularly important during longer payoff timelines when motivation can decline.Comparison Table: Budgeting Methods

Comparison Table: Avalanche vs Snowball Method

Who is this for?

Anyone currently carrying high-interest debt (credit cards, personal loans, payday loans)

People with multiple debts who need a clear system for deciding which to pay first

Households that feel stuck making minimum payments without seeing balances decrease

Individuals who want to eliminate debt before shifting focus to aggressive investing

Anyone who has tried to pay off debt before without a structured approach

FAQ

Should I pay off debt or invest first?

For debt above 7–8% interest (most credit cards, many personal loans), paying it off provides a guaranteed return equal to the interest rate. A credit card at 22% interest costs more than most investments return. However, contributing enough to capture a full employer 401(k) match is typically worth doing simultaneously — the match provides an immediate 50–100% return on your contribution.

How long does it realistically take to pay off significant debt?

It depends on the total balance, interest rates, and how much extra you can direct monthly. As a reference point, $50,000 in debt at 7% interest with $1,000/month in payments takes approximately 5 years. $100,000 at the same terms takes closer to 11 years. Adding even $200–$300/month extra can reduce these timelines significantly.

Is debt consolidation worth considering?

Consolidation can be effective if you can move high-interest debt (20%+) to a lower rate (8–12% personal loan or 0% balance transfer card). The key condition is that you stop adding new debt. Consolidation reduces interest costs but does not address the spending patterns that created the debt. It's a tool, not a complete solution. (Explore debt relief options)

Should I use savings to pay off debt faster?

Keep a minimum $1,000 emergency buffer. Beyond that, if you have savings earning 4–5% and credit card debt at 20–25%, the math supports using excess savings to eliminate the high-interest debt. The effective return on paying off a 22% balance is 22% — higher than most available savings or investment returns. Only do this if you commit to not re-accumulating the debt.

What about student loan forgiveness programs?

Programs like Public Service Loan Forgiveness (PSLF) and income-driven repayment (IDR) forgiveness can significantly reduce or eliminate student loan balances for qualifying borrowers. If you're potentially eligible, apply and track your progress. You may also want to explore refinancing if you have private loans or aren't pursuing forgiveness. (Compare student loan refinance rates | Compare student loan options) However, maintain a payoff plan alongside your forgiveness application — program requirements and policies can change, and having a backup strategy protects you from uncertainty. (Federal Student Aid: Loan Forgiveness)

Which debts should I focus on first if I have both credit cards and student loans?

Credit cards almost certainly have higher interest rates (18–25%) compared to student loans (4–8%). In most cases, prioritize credit card debt first. Student loans also often have more flexible repayment options (deferment, forbearance, income-driven plans) that credit cards don't offer, making them easier to manage while you focus on the more expensive debt.

Related Guides

The Order of Investing: Where to Put Your Money First — Where to direct your money once debt is eliminated

Emergency Fund Strategy: How Much You Actually Need — Why you need a $1,000 buffer before aggressive debt payoff

How Much Should I Invest Per Month? — Transition from debt payoff to wealth building

Sources

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation. Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you if you click through and take action. We only recommend products and services we believe are genuinely useful.