The Rule of 25: How to Know Your Retirement Number

The Rule of 25: How to Know Your Retirement Number

The Rule of 25 is a retirement planning formula that estimates how much you need saved to sustain your lifestyle indefinitely. You multiply your expected annual expenses in retirement by 25 to get your target portfolio size. The rule is derived from the 4% withdrawal rate: if you withdraw 4% of your portfolio each year, the math suggests your savings will last at least 30 years in most historical market conditions. It gives you a specific, actionable number to plan for.

TL;DR

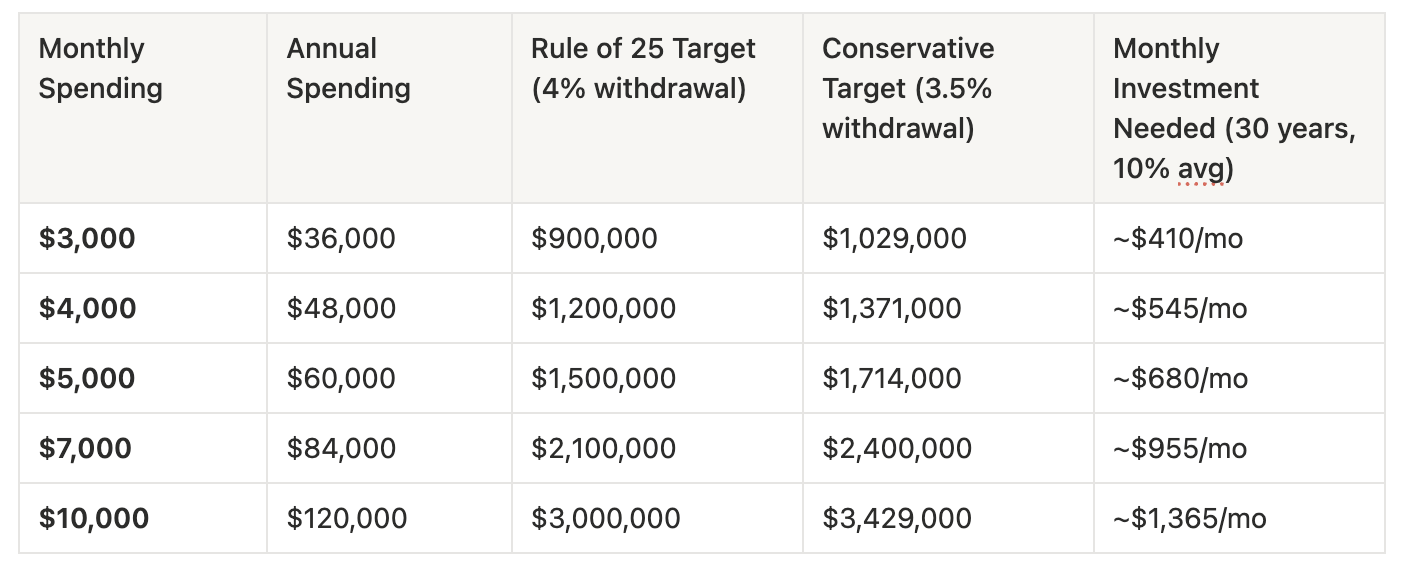

Take your expected annual expenses in retirement and multiply by 25. If you spend $60,000/year, you need approximately $1.5 million. If you spend $100,000/year, you need $2.5 million. This is based on the 4% withdrawal rule, withdrawing 4% of your portfolio annually has historically sustained a 30-year retirement in roughly 95% of market conditions tested. Once you know your number, work backwards to determine how much to invest monthly. Reducing expenses lowers your target, cutting $500/month in spending reduces your needed portfolio by $150,000.

The Framework

Calculate your annual spending. Add up your actual monthly expenses — housing, food, insurance, transportation, utilities, healthcare, and discretionary spending. Multiply by 12. This is the number that determines your retirement target, not your income.

Multiply by 25. $60,000/year x 25 = $1,500,000. At that portfolio size, a 4% annual withdrawal produces $60,000/year. According to the Trinity Study published in the AAII Journal, which analyzed rolling 30-year periods from 1926–1995, a 4% initial withdrawal rate adjusted for inflation had a roughly 95% success rate across stock/bond portfolio allocations. (Trinity Study — AAII Journal)

Work backwards to a monthly investment target. Once you have your number, use a compound interest calculator to determine your required monthly contribution based on your timeline and expected return rate. A $1.5 million target in 30 years at 10% average return requires approximately $680/month.

Understand that reducing expenses has a multiplied effect. Cutting $500/month from spending saves $6,000/year — but it also reduces your retirement target by $150,000 (since $6,000 x 25 = $150,000). Lifestyle inflation works in reverse: every dollar of unnecessary spending increases your required portfolio by $25.

Consider a more conservative withdrawal rate for longer retirements. The 4% rule was tested on 30-year retirements. For early retirees (retiring before 55), a 3.5% or 3% withdrawal rate provides additional margin. At 3.5%, multiply annual expenses by approximately 28.5. At 3%, multiply by 33.

Comparison Table: Retirement Numbers by Spending Level

Monthly investment figures assume 10% average annual return over 30 years. Actual returns will vary.

Who is this for?

Anyone who wants a specific, calculated retirement savings target rather than an arbitrary number

Investors who want to understand the relationship between spending, savings rate, and retirement timeline

People considering early retirement (FIRE) who need a framework for determining financial independence

Households that want to evaluate whether their current savings trajectory is on track

Anyone who finds retirement planning overwhelming and wants a simple, math-based starting point

FAQ

Does the Rule of 25 account for inflation?

The 4% withdrawal rule was originally tested with annual inflation adjustments built into the methodology. The Trinity Study modeled withdrawing 4% in year one, then adjusting that dollar amount upward each year for inflation. The 95% historical success rate includes inflationary periods. However, future inflation rates are uncertain, which is one reason some planners recommend more conservative withdrawal rates.

What if I want to retire early at 45 or 50?

The 4% rule was designed for approximately 30-year retirements. Retiring at 45 may require your portfolio to last 40–50 years. For longer time horizons, consider using a 3.5% withdrawal rate (multiply by 28.5) or 3% (multiply by 33). Research by Wade Pfau and others suggests lower withdrawal rates provide better survival rates for extended retirements.

Should I include Social Security in my calculation?

Social Security can reduce the amount your portfolio needs to generate. If Social Security provides $24,000/year and your expenses are $60,000/year, your portfolio only needs to produce $36,000/year — requiring $900,000 instead of $1,500,000. However, relying fully on Social Security projections decades in advance carries uncertainty. Many planners suggest calculating your number without Social Security and treating any benefits as additional margin.

Does paying off my mortgage before retirement change my number?

Significantly. If your mortgage is $1,800/month and it will be paid off by retirement, your monthly expenses drop by $1,800 — reducing your annual expenses by $21,600 and your Rule of 25 target by $540,000. Paying off housing costs before retirement is one of the most effective ways to lower your required portfolio. (Compare mortgage refinance rates | Compare home equity loans)

What if I don't know what my retirement expenses will be?

Use your current spending as a starting estimate. Many financial planners suggest retirees need 70–80% of pre-retirement spending, since some costs decrease (commuting, work clothing, payroll taxes) while others may increase (healthcare, travel). Starting with 100% of current expenses provides a conservative baseline.

Is the 4% rule outdated?

The 4% rule remains one of the most widely cited retirement planning frameworks. According to updated research from Morningstar and financial planner Wade Pfau, the safe withdrawal rate may range from 3.3% to 4.2% depending on asset allocation, time horizon, and market valuations at retirement. It's a starting framework, not a rigid rule. Adjusting withdrawals based on market conditions (spending less in down years) can significantly improve portfolio longevity.Related Guides

Related Guides

The $3 Million Retirement Math (Broken Down) — See the full math on what $500/month becomes over 40 years

How Much Should I Invest Per Month? — Work backwards from your Rule of 25 target to a monthly number

The Order of Investing: Where to Put Your Money First — The priority sequence for funding your retirement accounts

Sources

Trinity Study — AAII Journal: Retirement Savings Withdrawal Rates

Morningstar: State of Retirement Income (Safe Withdrawal Rates)

All content is for educational purposes only. Investing carries risk and past performance does not guarantee future results. This is not investing advice, specific recommendations, or legal advice. Consult a qualified professional for guidance specific to your situation. Some links in this article are affiliate links, meaning we may earn a commission at no extra cost to you if you click through and take action. We only recommend products and services we believe are genuinely useful.